There is a quiet but unmistakable shift happening inside the drawing rooms and boardrooms of India’s wealthiest families. The heir educated abroad, fluent in Bloomberg and private equity jargon, is coming home. But not to run the textile mill or the auto parts distributorship. He or she is coming home to run a family office.

Elders are calling it restlessness, or worse, ingratitude. We call it a macro-aware decision.

Some Numbers for you:-

India’s family office ecosystem has undergone a transformation that is difficult to overstate. From just 45 registered family offices in 2018, the country now hosts over 300, a more than 500% expansion in six years and counting. According to an EY–Julius Baer report, The Indian Family Office Playbook, this surge is not coincidental. It is being driven by something structural: a massive intergenerational wealth transfer estimated at ₹108 lakh crore over the next decade, and a younger generation that is looking at that wealth and asking a fundamentally different question than their parents did.

The older generation’s question was: How do I grow this business?

The younger generation’s question is: How do I grow this wealth?

These are not the same question, and we believe that’s a good thing given the profound change in our macro regime today.

Monetary Perspective

To understand why the next generation’s instinct is correct, you have to start with what central banks did during the pandemic and, more importantly, the second-order effect of their decision.

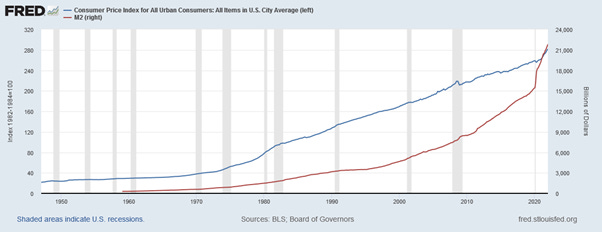

When the pandemic struck in 2020, policymakers across the world faced what they believed was a civilizational rupture. The response to that fear was simple: unprecedented monetary expansion. In the United States, the M2 money supply growth rate surged from approximately 5% in 2019 to 25% in 2020, the fastest increase ever recorded. The Eurozone was not far behind, with M3 growth jumping from 5% to approximately 12% in the same period, an annual flow of over €1.5 trillion, the fastest expansion since the euro’s inception.

The logic was reasonable at the time. If the economy were broken, you needed to flood it with liquidity to prevent a depression. The Fed cut rates to near zero, launched massive asset purchase programs, and bought nearly 90% of new mortgages created through GSE MBS between 2020 and 2022.

But here is where the story takes its critical turn: the economy was not broken.

Unlike the 2008 financial crisis, where credit channels were genuinely impaired, and the banking system itself was insolvent, the Covid shock was an exogenous supply disruption. Once vaccines arrived and restrictions lifted, consumer demand roared back. The economy proved remarkably resilient. Global GDP rebounded sharply. The corporate sector adapted. Labor markets recovered faster than almost anyone projected.

The money that was printed to fight an economic apocalypse found itself in an economy that had not, in fact, experienced one.

Where the Money Went

To understand the scale of what happened, consider this single data point: 45% of all US dollars ever printed in the country’s 250-year history were created in just two years, 2020 and 2021. The Federal Reserve, acting on the assumption that the pandemic had broken the economy beyond near-term repair, expanded the money supply at a pace with no historical precedent. What made this truly consequential was not the size of the expansion alone, but what happened next: it was never reversed. While the Fed raised rates aggressively from 2022 onwards, the stock of money in the system never contracted meaningfully. The monetary base built in those two years became the permanent floor and then continued climbing.

Capital, as it always does, followed the path of least resistance, and that path led directly into financial assets. An economy flooded with liquidity but not structurally broken did not absorb that money into productive capacity alone. It pushed into equities, real estate, private credit, and every asset class with a yield or an appreciation story attached to it. What we are living through today is not a cycle. It is the compounding effect of a one-time, never-reversed monetary event and the families that understand this are positioning accordingly.

Between the beginning of 2020 and early 2022, US households gained over $18 trillion in wealth, of which nearly 80% was driven entirely by asset price revaluations, not new savings or debt paydown, per Federal Reserve data. Equities generated a net gain of 23% for the S&P 500 from the start of 2020 through early 2021 alone. Real estate values soared, creating $9 trillion in owner-occupied housing wealth in just two years. Global equity grew at twice the rate of GDP from 1995 to 2021. From 2000 to 2021, the global balance sheet, the total of the world’s assets, liabilities, and wealth, quadrupled in dollar value, expanding far faster than the real economy it was supposed to be serving.

This was not a temporary distortion. It was, and continues to be, the defining feature of the investment landscape. Monetary policy created a structural bid underneath asset prices. And even as central banks subsequently tightened, raising rates aggressively from 2022 onwards, the long-run effect of a dramatically expanded money base has not been reversed. It has simply been redistributed.

The lesson for wealth-holders is stark: the most effective form of wealth compounding in this era has not been building things. It has by owning assets

The Velocity Problem

There is a second, less-discussed macro force that makes running a business harder.

As the post-COVID monetary expansion collided with supply chain disruptions and a reopening economy, inflation did not simply affect consumer prices. It worked its way into the cost structure of every business: wages, raw materials, logistics, energy, and real estate. According to the Federal Reserve Bank of New York’s Liberty Street Economics, businesses reported cost increases of approximately 5% in 2024, accelerating to 7% for service firms and 8.5% for manufacturers in 2025 well above their own prior year expectations.

This is not a blip. It reflects the rising velocity of money, money circulating faster through the economy as transaction volumes increase and financial intermediation deepens. When velocity rises, it acts as an amplifier: the existing money supply becomes more inflationary in effect, and the cost of goods and services required to run and expand a business rises at an accelerating rate.

The implications for capital-demanding businesses are severe. Every new unit of capacity requires more capex than before. Every incremental sale requires more working capital. Every new employee costs more to hire and retain. Margins compress not because demand is weak, but because the input costs chase revenue growth. Expansion, in this environment, is a treadmill you run faster just to stay in place.

The next generation sees this clearly. They are watching their family businesses pour capital into sustaining their competitive positions and wondering: is there a better use of this money?

The IPO Signal: Capital Markets Rewarding the Exit

India’s capital markets have, with uncanny timing, provided the answer.

India has undergone one of the most remarkable IPO booms in global history. In 2024, 227 IPOs raised a combined $12.2 billion in just the first eight months. The BSE and NSE hosted 30% of all global IPOs in 2024. Nearly ₹3.4 trillion was raised through mainboard IPOs in the two-year period of 2024–25 alone, more than half of the total ₹6 trillion raised in the 35 years between 1989 and 2023, according to Business Standard.

Read that again. More capital has been raised in two years than in the preceding three-and-a-half decades.

It is a message from the market itself: the value of your established, profitable business is at a peak relative to what it will cost you to run and grow it. The promoter who takes their business public today is converting an operating asset with all its attendant risks, capex requirements, and cost pressures into a financial asset that participates in exactly the kind of asset price appreciation described above.

The IPO boom created seven new billionaires in India in 2024 alone. Hyundai Motor India’s $3.3 billion listing was the largest in Indian history. Legacy consumer businesses, manufacturers, and financial firms all monetised at valuations that would have seemed fantastical a decade prior. Promoters who chose to list were, knowingly or not, executing a macro trade of exceptional elegance: selling operating leverage and buying financial leverage.

This is also not an India specific theme, look at the IPO sizes in the US today:–

The Asymmetric Advantage of Already-Built Wealth

There is one category of asset holder who sits in the ideal position in this regime, and this is perhaps the most important insight of all.

It is the business owner or their inheriting family whose core enterprise requires no further capital expenditure.

An established business with stable cash flows, a defensible market position, and no need for major new investment is insulated from the rising cost of capital. It does not need to borrow at higher rates to build new factories. It is not exposed to the capex treadmill that inflation creates for growth-oriented competitors. Its equity participates in broad asset price appreciation through re-rating of listed peers, through the general uplift in enterprise values, and through the wealth effect that flows through the economy.

Meanwhile, the family that has taken some or all of its wealth into a professionally-run family office can deploy capital dynamically into listed equities, alternative investments, pre-IPO opportunities, and real assets, precisely those categories that benefit from an expanding monetary base and rising asset prices. Family offices are already demonstrating this sophistication: according to India Briefing, Indian family offices contributed around 30% of the projected $100 billion raised by Indian startups, with many reaping significant returns from pre-IPO bets.

The next generation, managing capital rather than operations, is not stepping away from wealth creation. They are stepping toward the part of the value chain that the macroeconomic environment is currently rewarding most.

The Mandate

This shift is not unique to India, though India’s scale and pace make it particularly vivid. The UBS Billionaires Ambitions Report 2025 found that 82% of global billionaires now want their heirs to develop independent success, with only 43% expressing a desire for children to continue the family business a significant change from dynastic norms of prior generations. Globally, close to $84 trillion in wealth is expected to transfer to younger investors over the next two decades, per Capgemini’s World Wealth Report 2025. These inheritors, the research shows, will allocate more aggressively to alternative investments, private equity, and higher-growth asset classes.

What makes this generation different is not that they are less ambitious than their parents. It is that they are actually correctly reading the regime they are operating in. In a world where monetary policy has structurally inflated financial asset values, where the cost of running an operating business rises with increasing velocity, and where capital markets offer liquidity and exit at historically favourable valuations, the rational allocation of human capital is toward managing that financial wealth, not adding more operating complexity to it.

Our View

At Pinetree Macro, we think about wealth through the lens of macro regimes. The regime that began in earnest after 2020, defined by excess liquidity, asset price inflation, rising input costs, and periodically elevated velocity of money, has not fundamentally reversed, even as interest rates were raised. The stock of money in the system remains vastly larger than it was pre-COVID. The asset base on which financial wealth is built remains re-rated upward.

In this regime, the family that manages its wealth through a thoughtfully structured family office with professionally managed investment mandates governance, and correct exposure to financial assets, is not playing a different game than the family that runs a business. It is playing the same game, but with a great tailwind at its back.

The next generation who chose to build family offices instead of running factory floors are not idealists or financial dilettantes. They are, whether they know it explicitly or not are macro-aware who have intuited something fundamental about the world they have inherited.